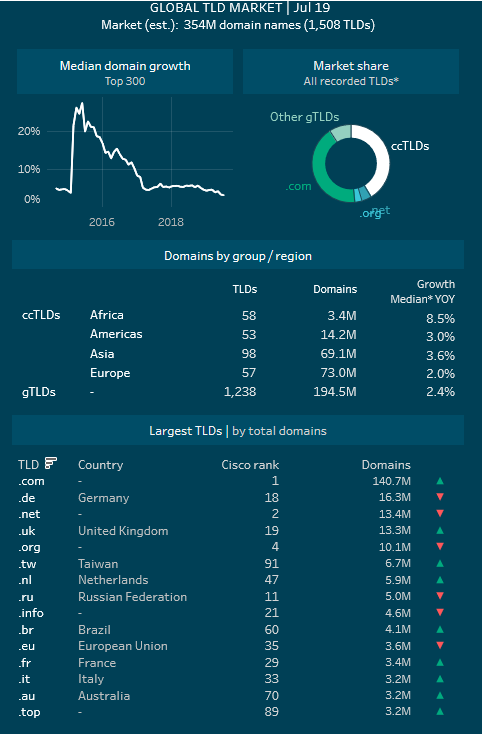

The heady days of double-digit percentage growth in the domain name industry appear to be over forever as the industry matures and in many markets registrations reach what appears to be saturation levels. The latest CENTRstats Global TLD Report Q2/2019 reflects these trends, although there are still areas of significant growth with .com continuing to show considerable growth along with African ccTLDs, although these are coming off a low base.

For the second quarter in a row, the report notes median

growth in the global domain name registrations hit a new recorded low. The

median growth of the 300 largest TLDs for the year to the end of June was 3.1%,

down from 5.6% a year earlier. Of the current top 300, roughly one-third have

contracted in total domains under management over the past 12 months.

Across regions and TLD types, the report shows growth rates range from 2.0% median among European ccTLDs to 8.5% among the relatively small number of African ccTLD domains. Since the beginning of the year, there has also been a noticeable drop in growth of gTLDs with the rate slipping from 5.0% to 2.4% YOY (based on the top 300).

New gTLDs (those launched from 2012 onward) which total well

over 1,000 different extensions, many of them for .brands and naturally with

relatively few registrations, have just under 10% of the market with a median

growth rate of 2.8% year-on-year. ccTLDs make up roughly 41% of all domain

registrations while .com, the single largest TLD, has a stable market share of

42%.

By region, Africa’s 58 ccTLDs had the largest growth rate

for the year to the end of June of 8.5%, bringing their total to 3.4 million

domain names across a continent of 1.2 billion people. Asia had the next

highest growth rate, growing 3.6% for the year to 69.1 million across its 98 ccTLDs

while the Americas 53 ccTLDs grew 3.0% to 14.2 million and Europe’s 57 ccTLDs grew

2.0% to 73.0 million.

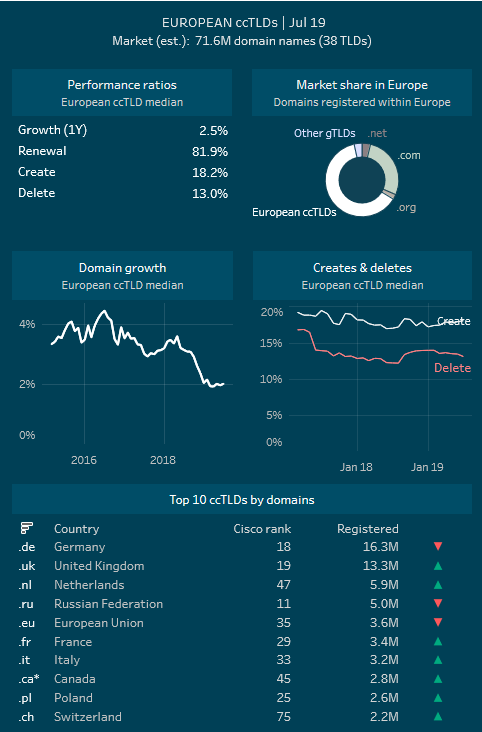

Among Europe’s 57 ccTLDs there are roughly 73 million domain

names. The report notes that after a particularly sharp slide in growth rates,

the past few months have seen a recovery pushing up from a low of 1.5% in April

to 1.9% (year-on-year) to the end of June. Growth is a direct result of the gap

between the create and delete ratio of a TLD (the larger the gap, the higher

the growth). This year as the report notes, the gap has clearly widened, driven

by increasing creates and decreasing deletes. This trend is an encouraging

signal for ccTLDs in the region since it suggests recent growth has been less

reliant on domain promotions which tend to yield short-lived benefits.

In terms of domain growth, high performing ccTLDs over the

past 12 months were .pt (Portugal), .ie (Ireland), .ee (Estonia) and .fr

(France).

Market share indicators can provide an impression on uptake

and visibility of different classes of TLD. European ccTLDs have an estimate

share of 63% based on registrations made within Europe. When based on Alexa

site ranks, the situation is similar with 65% of unique sites being European

ccTLDs. Although actual traffic to global sites such as google.com and facebook.com

can often be much higher than ccTLDs, the visibility of different European

ccTLDs based on these figures remains strong. When analysing country level

market share, local ccTLDs have a median of 54% of local registrations and 32%

of sites in the country’s Alexa top 1000 ranking.

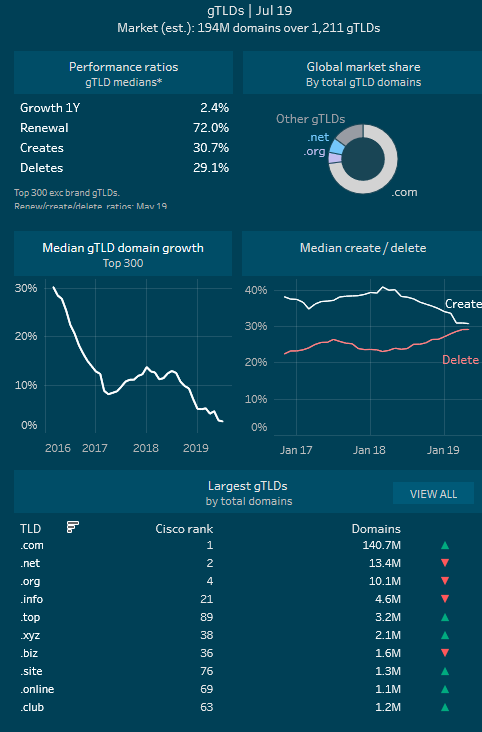

Growth among the gTLDs has continued to fall. The report shows median domain growth among gTLDs, legacy and new, has continued to fall and for the year to the end of June median growth was 2.4%. The rate has been driven by a closing gap between creates, which are reducing and deletes, which are increasing. Despite the slowdown, .com continues to achieve an above-average growth of 5.0% and a renewal rate of 71% which has helped to increase its overall gTLD market share to 73%.

On analysis of key performance ratios, a couple of new gTLDs

stand out. .blog has been growing steadily since late 2016 with domains under

management currently over 200,000, a relatively strong renewal rate of close to

60% and parked domains ratio (24%) well below the average. The long-term delete

ratio however has been slowly rising.

Another new gTLD worth noting is .shop. It has close to 700,000

domains and growth of 24% year-on-year. While the renewal rate is not high, the

report notes it is still very much in a growth phase with high relative create

ratio of 65%, which is well above the average.

Other strong performers in the mid-size category have been

.cloud, .life, .rocks, .tokyo and .world. Each of these gTLDs have strong

growth, relatively good renewal rates and low to medium rates of parking.

To download the latest CENTRstats Global TLD Report Q2/2019, go to: https://stats.centr.org/stats/global

This latest Domain News has been posted from here: Source Link